Give your team better health benefits in minutes.

Onboard securely and quickly, integrate your payroll systems, and start offering better benefits with Venteur.

Tell us your team’s unique needs

Define your desired contribution and share your employee roster. We’ll show you what coverage looks like for your team and you can adjust your budget accordingly.

Set up your HR and finance systems integration

We’ll integrate with your payroll and finance systems to make things flow seamlessly. Experience the ease of managing your benefits alongside your financial systems, all in one place.

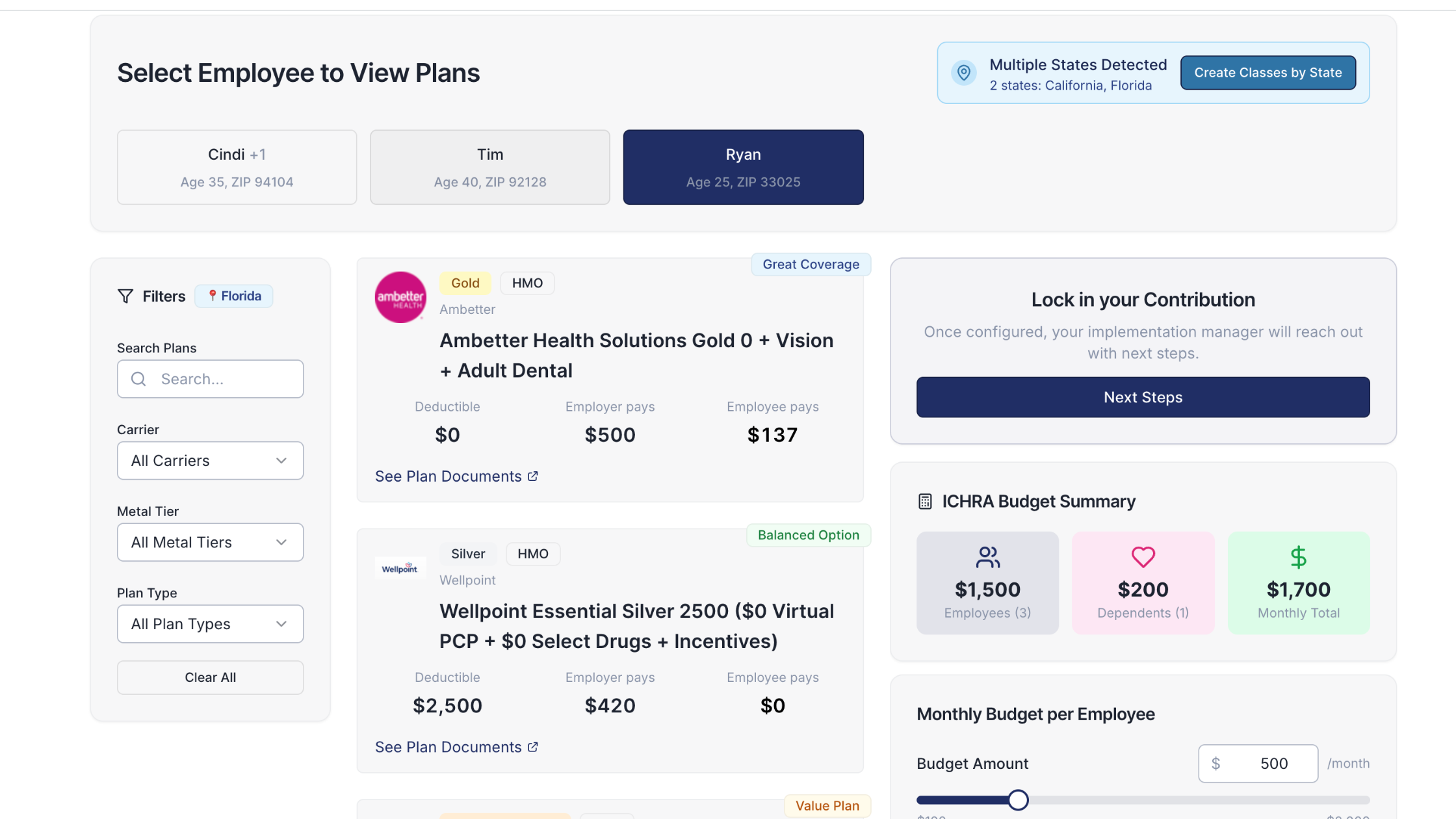

Manage your plan in the admin dashboard

Easily manage your benefits plan using Venteur's admin dashboard. Access all your plan details, make adjustments to your roster, and track usage efficiently.

.webp)

Reimbursements are simple and painless

We handle premium payments and reimbursements. Venteur’s Health Wallet makes it simple to submit and track reimbursements for any qualified health expenses.

And getting started is easy

Sign up

Begin your journey with Venteur by signing up effortlessly on our intuitive platform, where you'll gain access to a world of streamlined benefits management.

Dial in your plan

Take control of your benefits strategy with Venteur's user-friendly interface, allowing you to dial in your plan with precision and flexibility, ensuring it aligns perfectly with your company's unique needs and goals.

Launch to your employees

Launch your meticulously crafted benefits plan to your employees through Venteur's platform, providing them with immediate access to comprehensive coverage and resources tailored to their well-being.

You got questions, we got answers!

We're here to help you make informed decisions on health insurance for your business. Check out our FAQs or contact us if you have any additional questions.

ICHRA stands for Individual Coverage Health Reimbursement Arrangement (ICHRA). This health arrangement allows you to pick your own health insurance plan using your employer’s monthly tax-free allowance. These funds can be used to cover insurance premiums, including dental and vision, as well as qualified medical expenses.

What are the benefits of an ICHRA?

- Your health plan belongs to you, and you can keep your health insurance if you leave your company.

- You get to choose from any qualified health plan on the market. Venteur can help you select a plan where your preferred doctors, providers, and prescriptions are covered.

- If you choose a health plan that costs less than your employer contribution, the extra funds are added to Venteur’s Health Wallet, an account used to pay for qualified medical expenses.

Group health insurance plans are purchased by companies and offered to their employees. Traditional group plans take a one-size-fits-all approach to healthcare, giving employees limited choice when it comes to their coverage options. Employer-sponsored ICHRAs give employees a tax-free allowance to pick any plan on the public exchange that meets their unique needs.

Our sales team will discuss available options, helping each employer choose the best partner for their team.

1. What Your Health Wallet Balance Represents:

Your Health Wallet balance could be thought of as a measure of the medical expense reimbursements you're entitled to under your health insurance plan. It's essential to note that it isn't quite like a bank account with a set amount of accessible cash. Rather, consider it as a marker of what you're eligible to get reimbursed for as part of your ICHRA plan.

When you shop for insurance through the app, you will see a dollar amount that is available for out-of-pocket expenses. This amount is what gets contributed to your Health Wallet account for your use in reimbursements. However, depending on how your employer has setup the account, it may be available immediately or it may be available after every monthly invoice.

2. Your Health Wallet Account:

When your account is setup, there is a predetermined way on how your Health Wallet functions for your reimbursement funds. The first scenario is that there is money that has been set aside at the start of the period which can be used for your reimbursements. You may see the entire amount entitled to you is immediately available for medical expense reimbursements. It's like having a store of health benefits ready to be used when you need them.

3. Simplifying the Health Wallet Experience:

We're always striving to enhance your experience and are currently working on making the Health Wallet balance operate more like a pre-paid debit card. This shift aims to streamline the funding process further and allow you quicker and more direct access to your health reimbursements, leading to an even smoother journey for you.

Remember, whether your account shows the funds immediately or after every invoice, it doesn't affect the overall sum you're entitled to under your ICHRA plan; it merely affects the timing of when you will receive the reimbursements.

Your trust is important to us, and we're continually striving to make our services better for you. If you ever have questions about your Health Wallet or anything that would help make for a more understandable benefits experience with us, don't hesitate to reach out to our customer service team.

The Affordable Care Act (ACA) requires that employers with more than 50 full-time equivalent employees provide health insurance to their employees. This is known as the 'employer mandate'.

ICHRAs can meet the mandate as long as they are considered 'affordable.' According to IRS, 'an ICHRA is affordable if the remaining amount an employee has to pay for a self-only silver plan on the exchange is less than 8.39% of the employee’s household income.'

To simplify, this means that the ICHRA contribution an employee receives cannot be less than the lowest-cost silver plan available to the employee - (9.02% of the employee's household income).

%20eligibility%20FAQs.avif)